New York, New York

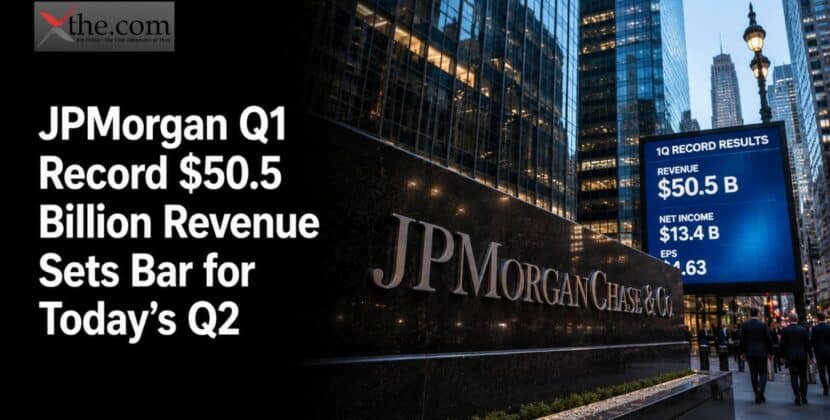

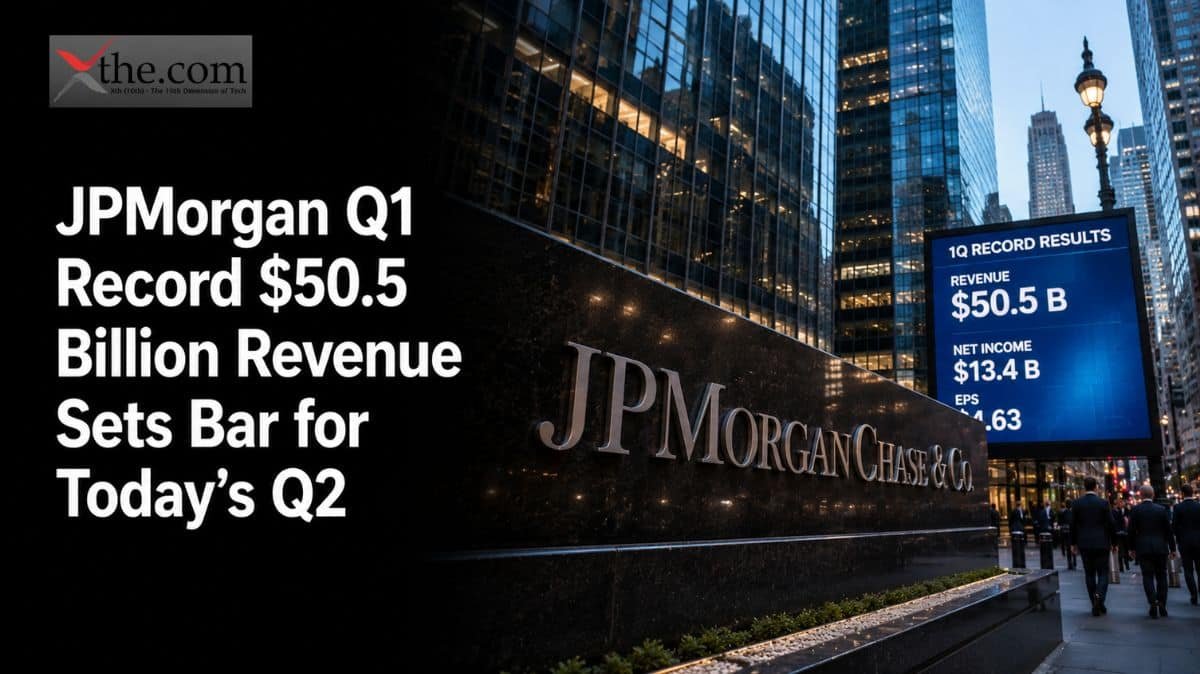

One quarter changed expectations across the banking sector. When JPMorgan Chase reported $50.54 billion in managed revenue for the first quarter, it beat estimates by more than $2 billion and prompted analysts to revise their models for the rest of the year. Now the reckoning has arrived. JPMorgan Q2’s earnings on July 14 land before the opening bell, and the question looming over trading desks is simple: can the bank match a quarter that even its executives called exceptional? The JPMorgan Q1 record revenue figure set a high standard, and today’s results will show if that was a one-time peak or the start of a new trend.

The $50.54 Billion Baseline

Numbers don’t consistently tell the whole story, but JPMorgan’s first quarter came close to speaking for itself. JPMorgan’s Q1 $50.54 billion record revenue was up 10% year over year, alongside net income at $16.5 billion and earnings per share of $5.94, beating Wall Street’s $5.45 estimate. All major business lines contributed. The Commercial and Investment Bank saw revenue grow by 19%, and return on tangible common equity hit 23%, a level most regional banks can only hope to reach after years of growth.

FICC Led the Charge

Fixed income trading rarely grabs headlines outside of earnings season, but this quarter it did the heavy lifting. JPM FICC 21 percent Q1 growth pushed that desk’s revenue to roughly $7.08 billion, the strongest showing in years. Institutional clients spent the quarter hedging against tariff whiplash, rate uncertainty, and a jittery Treasury market, and JPMorgan’s trading floor captured a large share of that activity. Combined with equities trading, total Markets revenue hit a record $11.6 billion, nearly $2 billion above the previous high.

Investment Banking Roared Back

After two slow years, dealmaking finally picked up again. JPMorgan’s investment banking 28 percent, raising fees to $2.88 billion, mostly from advisory work and equity capital markets. Companies that had put off acquisitions in 2024 and 2025 started making deals again, and JPMorgan’s bankers benefited. This was the strongest sign yet that the M&A slowdown was over.

Net Interest Income Held Its Ground

The bank’s oldest and steadiest business also delivered. JPMorgan’s net interest income was $25.5 billion for the quarter, up 9% from last year, even as the Federal Reserve’s rate outlook became less clear. Average loans increased by 11% to $1.5 trillion, and deposits grew by 7% to $2.6 trillion, giving the bank a larger base for earning spread income. CFO Jeremy Barnum slightly lowered the full-year net interest income forecast, from about $104.5 billion to $103 billion, briefly unsettling the stock during an otherwise strong quarter.

What Wall Street Wants from JPM Stock Q2 Results

Analyst models heading into today diverge on magnitude but agree on direction. Consensus estimates place second-quarter earnings per share between $5.44 and $5.61, and revenue around $48.6 to $49 billion. That’s lower than the first quarter’s results but still a solid year-over-year gain. JPM stock Q2 results will be less on whether JPMorgan beats expectations and more on the tenor of the report. Options suggest the stock could move 4.4% on the day of the release, which is a bigger swing than usual for a stock near its 52-week high. Investors who have bought JPM shares this year—up about 18.6% over the past year—are not likely to tolerate much disappointment at these prices.

The outlook for net interest margin is key. If the Fed keeps suggesting lower rates, JPMorgan’s spread income could shrink even if loan volumes rise. Another cut to full-year net interest income guidance, after the April reduction, would probably unsettle the stock, no matter how strong trading revenue is. If guidance holds steady or goes up, it could restart the rally that slowed after the first quarter.

The Hormuz Wildcard

Geopolitics usually doesn’t affect bank earnings reports this directly, but the shipping problems in the Strait of Hormuz are now too big to ignore. The conflict with Iran affects JPMorgan in two ways. It creates the kind of market volatility that boosts trading revenue, especially in energy and currency markets, as in the first quarter. But it also creates risks for JPMorgan’s energy-related loans, since higher costs and shipping delays can put pressure on borrowers who were in good standing not long ago.

Jamie Dimon has been warning about a complicated risk environment for several quarters, and today’s call will likely include new comments on how the bank sees credit quality in this context. Investors should pay attention to whether Dimon describes the Hormuz-related volatility as a positive for trading, a negative for credit, or both. His outlook frequently influences how the whole banking sector trades that day.

What to Watch When JPMorgan Reports Today

Three things are more important than whether JPMorgan beats expectations. First, watch the full-year net interest income guidance—a second cut would show that rates are hurting more than management admitted before. Second, look at the net interest margin, which reveals if the spread of business is getting tighter or looser. Third, look for any specific numbers on credit reserves in energy or shipping-related loans, since that’s where the Hormuz disruption would first appear in the bank’s finances.

Anyone searching for “JPMorgan Q2 earnings July 14, 2026, what to expect to record Q1 $50.5 billion” really wants to know if the bank’s strong balance sheet—a term Dimon often uses—can withstand both trading gains and credit risks coming from the same event. The first quarter showed it could. Today’s results will be revealed if that continues.

A Preview Worth Watching Live

For traders wanting to follow the release as it happens, “JPMorgan Chase Q2 2026 results FICC NII investment banking preview today” is one of the top search terms this morning, and it’s easy to see why. JPMorgan’s earnings start the whole bank reporting season, with Goldman Sachs, Bank of America, Wells Fargo, and Citigroup all reporting on the same day. The June Consumer Price Index report also comes out that morning, adding big-picture economic data to company results.

What happens between 7:00 a.m. and the market open will shape investors’ view of bank earnings for the rest of the quarter. If JPMorgan’s trading desks took advantage of Hormuz-driven volatility and credit quality stayed strong, the stock will probably keep rising in 2026. But if net interest income guidance drops again or credit costs go above the $2.5 billion set aside in the first quarter, expect a tougher day for the stock. Either way, the record JPMorgan set in the first quarter is no longer only a benchmark—it’s now the standard the bank has to meet.

Source: JPMorgan Chase (JPM) Q2 Earnings Report Preview: What To Look For