Washington D.C.

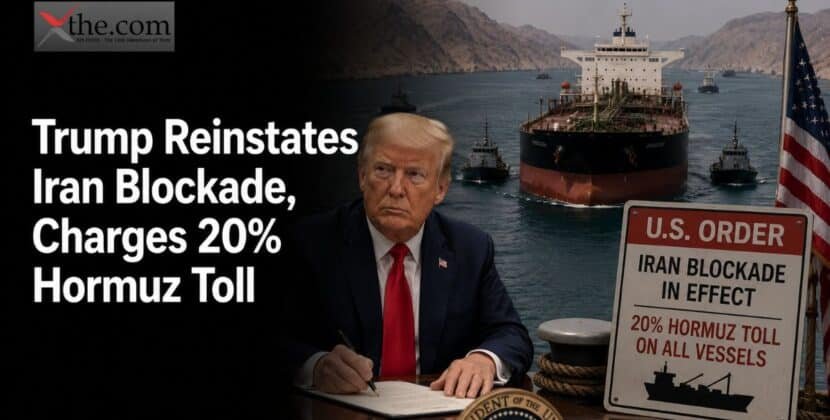

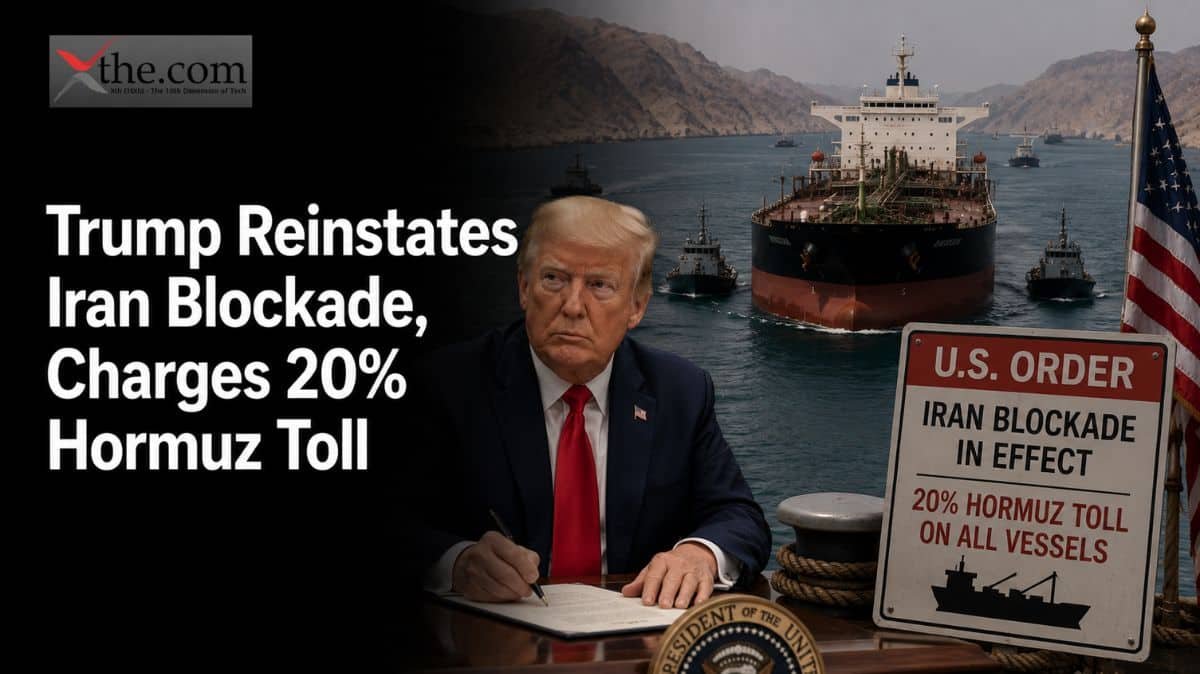

Oil traders had exactly one Monday morning headline to digest, and it moved every desk on Wall Street before the opening bell finished ringing. Trump Iran blockade reinstated — four words that, within hours, added roughly two dollars to a barrel of crude, knocked chipmakers into the red, and forced bond traders to rethink inflation risks for the rest of 2026. President Trump said the Strait of Hormuz blockade was back in place for Iranian shipping and paired it with something no American president has attempted before: a Hormuz 20 percent toll on every other ship passing through the waterway.

The details are more important than the headlines. About one-fifth of the world’s seaborne oil and a similar amount of global liquefied natural gas move through this 21-mile-wide channel between Iran and Oman. A 20 percent surcharge on that much cargo is more than just for show. It acts as a tax on global energy logistics, set by the U.S. alone, with enforcement rules still being figured out as events unfold.

What Trump Actually Announced

Trump posted from the White House that the United States would now be called Trump Guardian of the Hormuz Strait, using his own phrase and stressing it to underline the point. He wanted to present the toll as fair compensation, not extortion. “As a matter of fairness,” he wrote, the U.S. should be paid back for keeping the passage secure. He did not say how the toll would be collected, who would handle payments, or whether Gulf allies were consulted before the announcement.

At the same time, Trump confirmed that Iran ships ‘ Hormuz-blocked status had returned. The blockade targets vessels registered in Iran or carrying Iranian cargo, bringing back a rule that had been paused during the ceasefire in mid-June. That ceasefire had stopped Tehran from charging its own transit fees. Iran did not fully follow the agreement, and after a container ship was attacked in the strait last week, Trump said the truce was “over.” The Islamic Revolutionary Guard Corps had already said the strait was closed to foreign ships, but Trump responded that it was open, though only under American rules.

The Legal Basis Trump Is Leaning On

No current treaty allows a country to impose a cargo toll on an international strait on its own. The 1982 UN Convention on the Law of the Sea guarantees ships can pass through such straits, and while the U.S. never officially joined the convention, it has usually followed these rules. Instead, administration officials point to the president’s war powers and a July 10 letter Trump sent to Congress, saying U.S. forces started new operations against Iran on July 7. With this reasoning, the toll is described as a means of recovering costs for a military campaign that secures the shipping lane, not merely a maritime fee. However, maritime law experts doubt this argument works outside of a war context, since the toll affects ships with no link to Iran or the conflict.

Which Nations Feel It First

The toll hits the hardest in countries that cannot easily find other routes. Japan and South Korea obtain most of their crude oil through the Strait of Hormuz and lack reliable pipeline alternatives. China, the biggest buyer of Gulf crude, must either pay the surcharge or deal with long delays by rerouting around the Cape of Good Hope. India’s refiners, who had relied on cheaper Gulf oil during the conflict, now face a toll that removes the price advantage. European buyers, who have already shifted toward U.S. and West African crude since 2022, are less affected. Shipping analysts have identified who stands to gain from a policy aimed at Iran.

How Markets Reacted

By Monday’s close, the reaction was unambiguous. The S&P 500 fell 0.79%, the Nasdaq Composite dropped 1.55% as chip stocks led losses, and the Dow Jones Industrial Average — cushioned somewhat by energy names — still shed more than 138 points. Brent crude was the day’s most-watched instrument. Traders reached for shorthand almost immediately: Brent crude $82, Hormuz blockade became the phrase pinned to trading desks, though the benchmark’s actual print bounced across a wider band intraday, with some venues reporting a brief spike near $83 and others settling closer to $80, depending on the contract and the minute. Whatever the precise tick, the direction was consistent — a jump of roughly 5 to 9 percent from where crude sat just days earlier.

The bond market reacted too. The 10-year Treasury yield rose to 4.61% from 4.56% at Friday’s close. This increase suggests that investors expect higher energy costs to appear in this week’s inflation data, and that Federal Reserve Chair Kevin Warsh will have to address them when he speaks to the House Financial Services Committee.

The Economics of Every Cargo Vessel Now Routing Through the Gulf

For shipping companies, math changed overnight. One Very Large Crude Carrier carrying two million barrels, even at a modest $75 per barrel, holds about $150 million in cargo. A 20 percent toll on that shipment adds $30 million in costs—a figure not covered by current contracts and likely to be passed on to buyers, since carriers are already paying high war-risk insurance premiums. Some shipowners may decide to wait out the situation, keeping their tankers anchored in the Gulf of Oman instead of agreeing to a fee system with unclear rules and no end date.

This week, analysts searching for “Trump reinstates Iran blockade 20 percent toll Hormuz all cargo July 2026” mostly want to know whether the toll is just a starting point for talks or will become a long-term policy. Right now, no one outside the White House knows, and the White House has not given an answer.

What Comes Next

The first real test comes with Tuesday’s June CPI report and Warsh’s testimony in Congress, which will show how much of this shock the Fed sees as temporary. The phrase Trump 20% cargo toll July 14 is already making the rounds on trading floors and in procurement offices, and everyone involved in Gulf shipping—insurers, refiners, and government buyers—is now preparing for scenarios that were not on the table a week ago. Anyone following the situation with phrases such as “US Guardian Hormuz Strait 20% shipping fee Iran blockade investor impact” should expect continued volatility until Washington either establishes a formal mechanism to collect the toll or quietly drops the idea, as it has done with past proposals for Hormuz fees. Given how quickly things have escalated since February, expecting the idea to quietly disappear seems like the riskier bet.

Source: Stocks end lower as oil prices surge on renewed Hormuz tensions, SK Hynix leads chip stock sell-off